🧤 $100/ton CDR > Anything Else?

🧤 $100/ton CDR > Anything Else?

(118) [carbon] --> [ ] removal

Good Morning

What we’re reading this week:

Interview with Insolvent author discussing technology, sustainability, and social justice (TT)

Why Now Is the Best Time to Invest in Late-Stage Climate Companies (F)

How to maintain hope amid defeating climate change graph fatigue (WP)

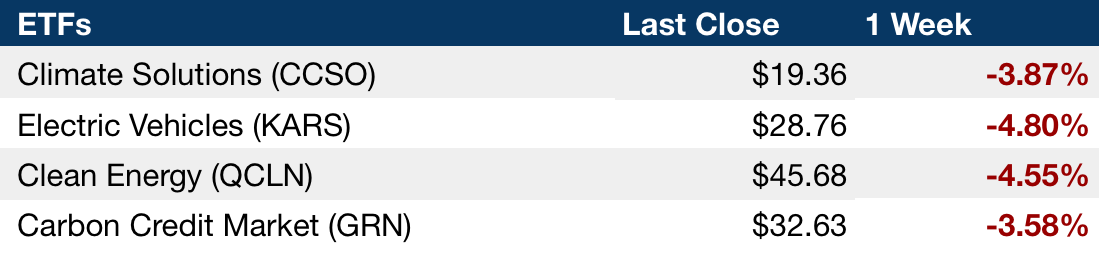

The Greendicator

Top Deals of the Week

H2 Green Steel, a Stockholm-based startup building a large-scale green steel plant, raised ~$1.6B in funding led by Altor, GIC, Hy24, and Just Climate(FN)

Ascend Elements, an eight-year-old startup based in Westborough, Ma., that is creating battery materials for EVs, raised a $460 million Series D round. Decarbonization Partners, Temasek, and Qatar Investment Authority co-led the deal. More here.

Avatr Technology, a Chinese smart electric vehicle company, raised 3 billion yuan ($411.5 million) in Series B funding. Participants included the Chongqing Industry Investment Fund of Funds (NA)

Boston Metal, a decarbonized metals technology solutions company, raised a $262M Series C from Aramco Ventures, M&G Investments, Goehring & Rozencwajg, and others (BW)

Ambient Photonics, a low-power solar startup for connected devices, raised a $30M Series A-2 led by Fine Structure Ventures (BW)

Nuventura, a six-year-old Berlin startup that builds equipment that is used to control the flow of electricity in power grids that does not use SF6, a greenhouse gas, raised a $26.8 million Series A round led by Mirova (TEU)

Paptic, an eight-year-old startup based in Espoo, Finland, that develops sustainable packaging materials, raised a $24.7 million Series A round led by European Circular Bioeconomy Fund. More here.

Solar energy startup Okra raised a $12M Series A led by One Ventures (TC)

Lydian, a CO2-derived fuels and chemicals startup, raised a $12M seed round led by Congruent Ventures and Galvanize Climate Solutions (FN)

Lumen Energy, a four-year-old San Francisco startup that helps commercial real estate owners evaluate their buildings and deploy clean energy technologies, raised an $11 million Series A round led by Ajax Strategies (A)

Spiritus, a two-year-old startup based in Zagreb, Croatia, that captures carbon dioxide through a series of filters and uses the captured carbon dioxide to create products such as fuels and plastics, raised an $11 million round led by Khosla Ventures. More here.

e-mobilio, a Munich-based provider of a cloud recommendation and buying platform for drivers to switch to electric mobility, raised a $10.2M Series A led by SET Ventures (FN)

Opna, a startup aiming to help companies hit ‘net zero’ by finding and funding carbon projects, raised a $6.5M seed round led by Atomico (TC)

Miami-based startup Kind Designs, making “eco-friendly sea walls to protect coastal communities from rising sea levels” (consider our eyebrows raised) raised a $5M seed round led by GOVO Venture Partners (BW)

Green Theory

Carbon Captors: Capitalization of Carbon Part II

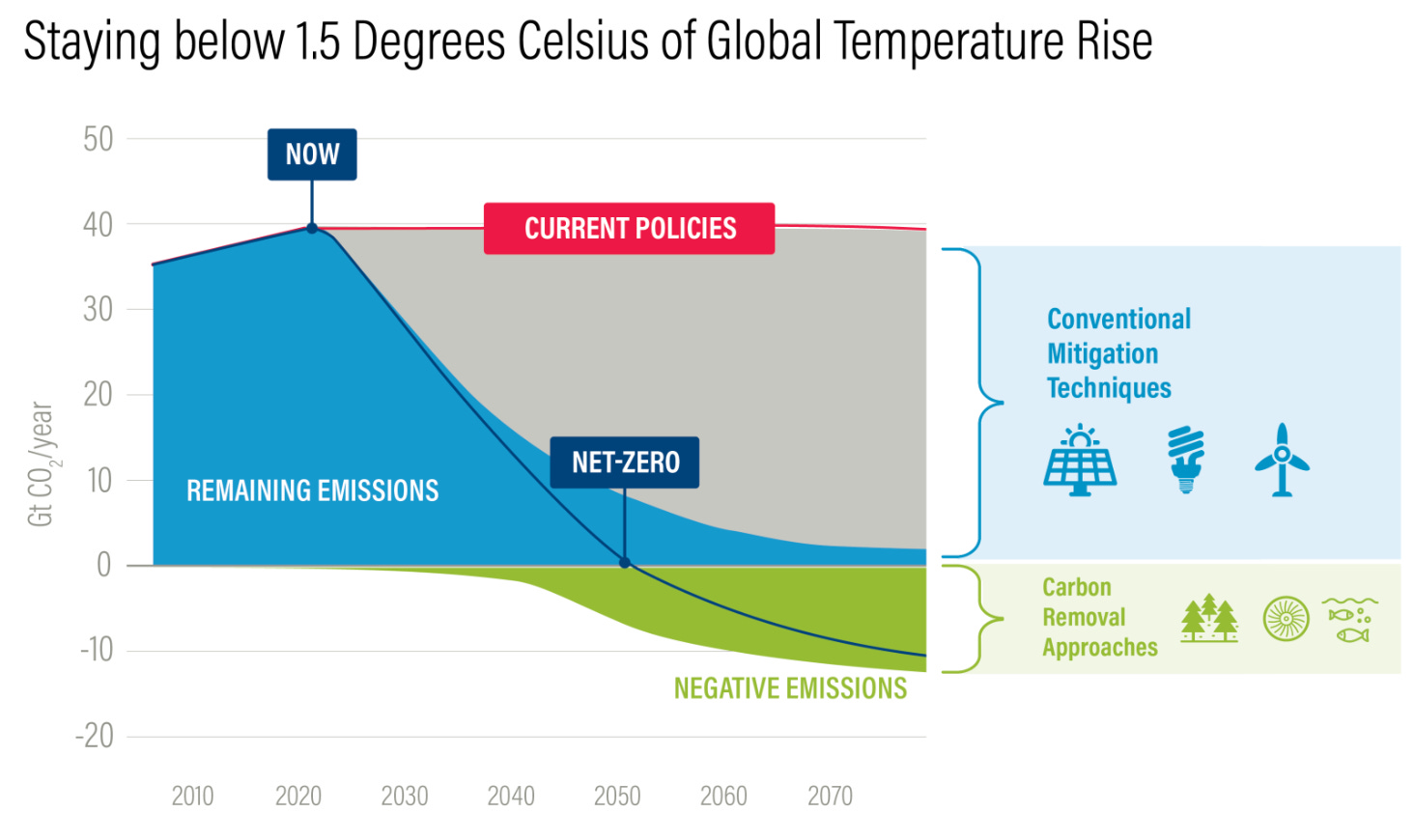

Some technologists have given up on reducing emissions by implementing cleaner technology, and focus instead on capturing emissions from the wild. These scientists and founders claim that we must invent and refine new technologies to reduce atmospheric carbon, since cutting emissions today won’t undo historical harms.

If we got emissions down to zero today, natural systems could still absorb the existing excess carbon and warming would be limited to the next few decades, according to Climate.gov. And yet, deep-pocketed venture capitalists and governments are pouring billions of dollars into carbon capture and removal.

Last week, we kicked off the capitalization of carbon by looking at just how dramatically human emissions have accumulated, and the actionable economic schemes to reduce emissions: tracking and regulating ongoing emissions. Carbon taxes and carbon markets, as discussed, don’t require any form of these technologies: carbon capture, sequestration, storage, and removal.

Instead of an economic model for reducing ongoing emissions, carbon capture—and associated geoengineering operations—are methods of physically altering the path of carbon through global systems. Who’s paying for these physical carbon services, and what’s the difference between them?

Capture, then…

Capture refers to the act of securing carbon that we’d otherwise expect to end up in the atmosphere. Once the carbon is captured, how long it stays that way is highly variable. For example, most CO2 capture is done by oil & gas companies, and then either sold to re-releasing industrial firms, or used in enhanced oil recovery, to pull more oil from the ground.

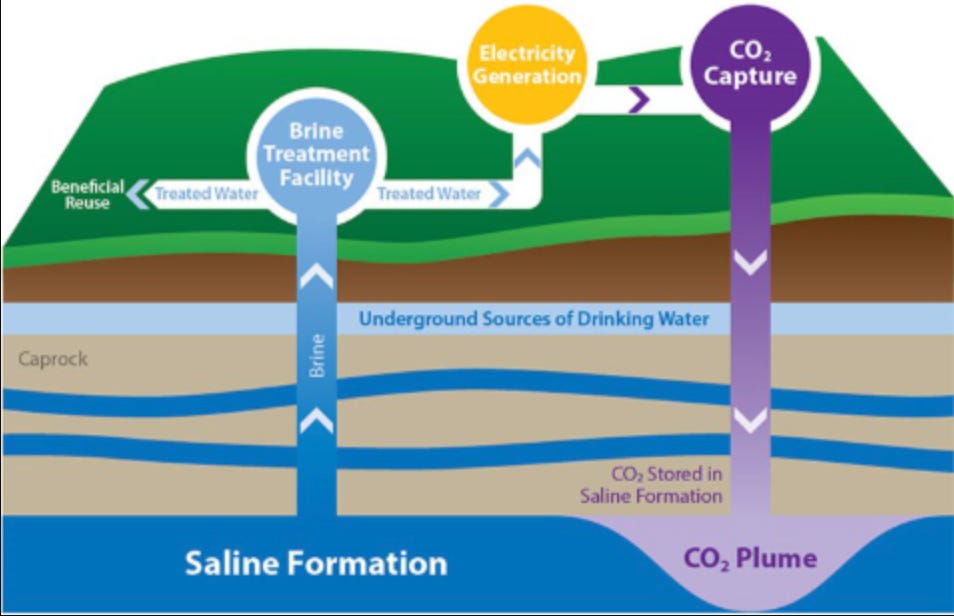

Still, many startups are boasting their own strategies of harnessing carbon dioxide. Take Carbon Engineering, a Canadian startup which operates direct-air-capture (DAC) facilities. After capturing carbon from the air itself, the startup advertises one solution for storing carbon geologically, and another for simply re-releasing it as fuel. Both offerings are considered carbon capture, since the company is pulling out existing emissions in each case.

Sequestration, Storage & Removal

When Carbon Engineering’s carbon is re-released as fuel, we start to see the difference between carbon capture, and its more stringent counterparts of storage, sequestration, and removal.

Releasing the carbon again means it is no longer stored, sequestered, or otherwise removed. While carbon capture could be used for immediate re-release, carbon sequestration refers to captured carbon that’s intentionally tucked away from atmospheric circulation. As the US Geological Survey explains, carbon may be sequestered in geologic formations (underground or beneath the seabed), or in biological systems (such as trees or seaweed).

We ought to expect sequestered carbon won’t re-enter the atmosphere, but biological systems are less reliable carbon sinks, compared with geologic formations. Further, even common methods of sequestration can in fact be tapped to re-release carbon later. In this case, carbon storage may be used instead of sequestration, but not always. Oil and gas companies are adept at carbon storage: injecting carbon underground, with the option to access it at a later time.

The most strict form of carbon capture is called carbon removal. When carbon is captured for removal, the captors claim to be permanently taking atmospheric carbon out of play (or at least for 50+ years). Some carbon sequestration or storage is lengthy enough to qualify as carbon removal, though not all.

Carbon removal startups are sprinting ahead of regulators, deploying unproven technology and drawing warnings from concerned scientists and ecologists, who criticize the poor incentives for genuine stewardship and honesty about accuracy, among other issues.

Cash-pture

Depending on where the carbon is destined, carbon capture may include sequestration, storage, or even removal: the longest-duration form of capture.

Who’s paying for all of this? Commercial buyers of captured CO2 are largely going to release it again, or use it to harvest yet further nonrenewable resources, and deepen our commitment to fossil fuel infrastructure. When we look more closely at companies such as Carbon Engineering, you’ll see even their “DAC + Storage” solution is used for enhanced oil extraction, making oil & gas companies a key customer.

Outside of the private markets, the federal government is building 4 carbon removal “hubs”, to capture a measly 4 million metric tons per year, when fully ramped-up. That’s the carbon equivalent of only 10 gas-fired power plants shutting down, or about 1% of the nearly 1,000 in the US.

If a company or individual is paying for carbon’s sequestration, storage, or removal, it’s purely voluntary. Do carbon removal buyers fund it to get rid of historical emissions—as carbon geoengineering advocates suggest is the entire purpose of their technologies—or do companies and people pay for carbon removal schemes to offset current sources emissions?

We’ll explore how these voluntary markets, including offsets and net zero, connect to carbon capture and removal, next week.

The Closer

This beauty is courtesy of USFWS