🌑 Purring thru perils: cat bonds

🌑 Purring thru perils: cat bonds

(149) Series A & B spree

Good Morning

What we’re reading this week:

Recent heatwaves are a harbinger of Africa’s future (E)

As California’s redwoods recover from fire, an astonishing fact emerges (SFC)

Bay Area hosts first-in-nation experiment to slow global warming — by helping clouds deflect sunlight (SFC)

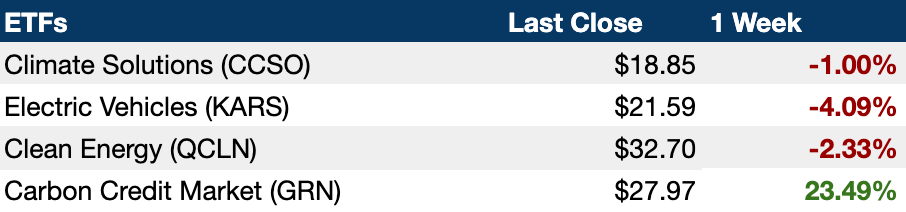

The Greendicator

Top Deals of the Week

HysetCo, a startup developing hydrogen-powered transportation solutions, raised $216M in funding led by Hy24 (EU)

Zero-emission truck developer Windrose Technology raised a $110M Series B led by HSBC New Economy Fund (PRN)

Arcadia, a global utility data and community solar platform, raised a $50M growth round from Macquarie Asset Management and more (PRN)

ION Clean Energy, a startup providing post-combustion point-source capture technology, raised $45M in funding led by Chevron New Energies (BW)

Methane-to-value startup Windfall Bio raised a $28M Series A led by Prelude Ventures (BW)

Kenyan solar irrigation startup SunCulture raised a $27M Series B from InfraCo Africa, Acumen Fund, and more (FN)

Sustainable packaging tech startup watttron raised a $13.3M Series B led by Circular Innovation Fund (FN)

Iceberg Data Lab, a startup measuring environmental data and providing environmental life cycle analysis, raised a $10M Series A led by Beringea (EU)

Carrar, a startup providing EV battery modules and thermal management systems, raised a $5.3M Series A led by Salida B.V., OurCrowd, and NextGear (BW)

Green Theory

Purring through Perils: Cat Bonds

In 1992, Hurricane Andrew struck Florida, and other communities hundreds of miles away. In addition to the staggering loss of life and record-breaking property damage, over 7 insurance companies became insolvent in the wake of the disaster. With the exposure of its underestimated and over-concentrated risks, the disaster insurance industry had to re-evaluate its shape and technical prowess.

")

{kind=link}

Today, when disaster strikes, modern finance relies on a new type of bond for backup: catastrophe bonds. These bonds have greatly expanded the capital available to disaster-prone businesses, homes, and public infrastructure, but will this novel asset class sustainably insure our built environment through coming decades of climate change?

Betting against destruction

When you buy a catastrophe bond, you agree to receive small interest payments over time. If no catastrophe occurs by the time your bond comes due, the issuer returns your initial investment to you. On the other hand, if your issuer or their client is imperiled by a natural disaster, you forfeit your initial investment, and lose everything.

Those buying catastrophe bonds will be quick to point out that they view themselves as betting against climate disasters, rather than on them. If you hold catastrophe bonds, you win when everything goes smoothly. Since 1997, only about 3% of all dollars put in catastrophe bonds have been lost in payouts. The rest earned interest, enriching bondholders across disaster assets.

Catastrophe bonds differ in their geographic scope and type of peril. Some bonds focus on state-level risks, while others look at entire countries or continents. When it comes to covered perils, wind and earthquakes are the most popular, with multiperil products and some fire assets gaining ground, too.

Parametric Paradise

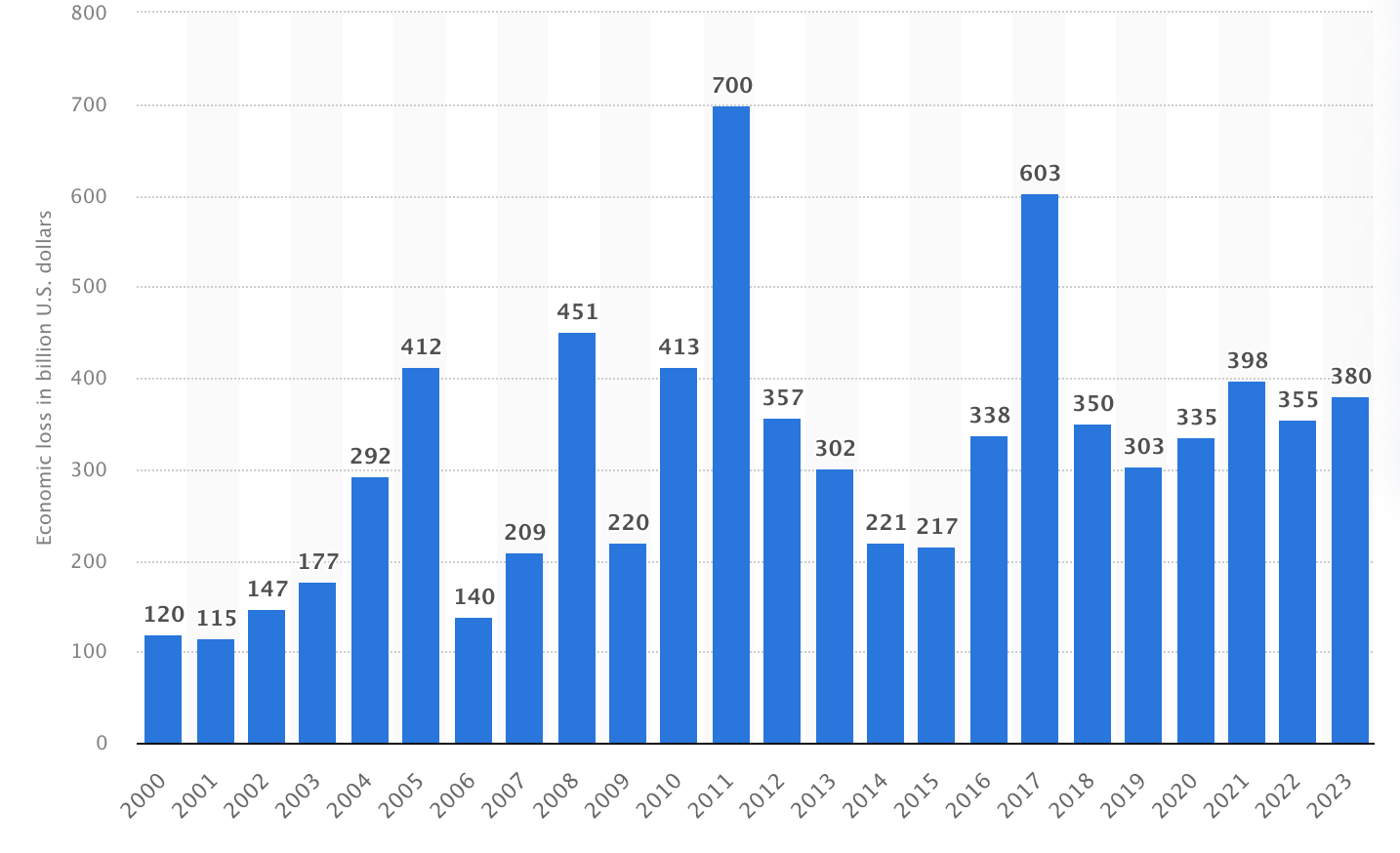

The entire catastrophe bond asset class totals over $40B, or roughly the amount of cash that Ford Motor Company keeps around. This portfolio only holds enough money to cover about 10% of the $380B in damages reported in 2023, but catastrophe bonds don’t need to pay out all damages to help with rebuilding.

Parametric insurance models offer a way to bet against a disaster with less downside risk, accelerating the growth of catastrophe bonds. Parametric insurance pays victims a set amount when a certain parameter is met, such as water rising above a certain level in a given area. Instead of indemnifying victims against all losses, parametric models may only partially cover the full financial impact of a disaster.

For all that parametric plans sometimes lack in coverage, they make up in speed. Instead of waiting weeks, months, or even years for investigators to evaluate the full extent of your damage and calculate losses manually, parametric insurance payments can get triggered by a simple sensor, and arrive in a victim’s bank account in mere hours.

New York City employed this model to insure the subway and tunnels, using public sensors to monitor the policy’s parameters in real time, alongside cat bond holders. Over time, this system has been expanded to protect business, and even homeowners, too. For those running small businesses, especially, reopening faster can have a serious impact on longer-term viability.

Companies such as FloodFlash offer low-cost sensors to extend the New York parametric model to commercial and public properties in the UK and several US states. Simply put, if the sensor gets wet, the insured gets their fixed payout. Though first codified and popularized in life insurance, parametric models keep pushing the insurance industry into new, more expedient arrangements.

Why would investors want catastrophe bonds?

Investors crave diversity. Catastrophe bonds, according to their advocates, are uncorrelated with traditional assets such as stocks, making them an appealing way to hedge against risk. Even though a large shock to the financial sector may result in widespread losses, catastrophe assets that remain profitable can help offset the downside.

Pension funds have been increasingly investing in alternative assets, such as catastrophe bonds. This change is driven in part by traditional public bonds offering lower returns in the wakes of central banks slashing interest rates to respond to crises, and deregulation of public pensions.

With society’s growing reliance on catastrophe bond returns, we all share in needing their risks and returns estimated accurately. So are these assets truly uncorrelated with the market?

Catastrophe-bound

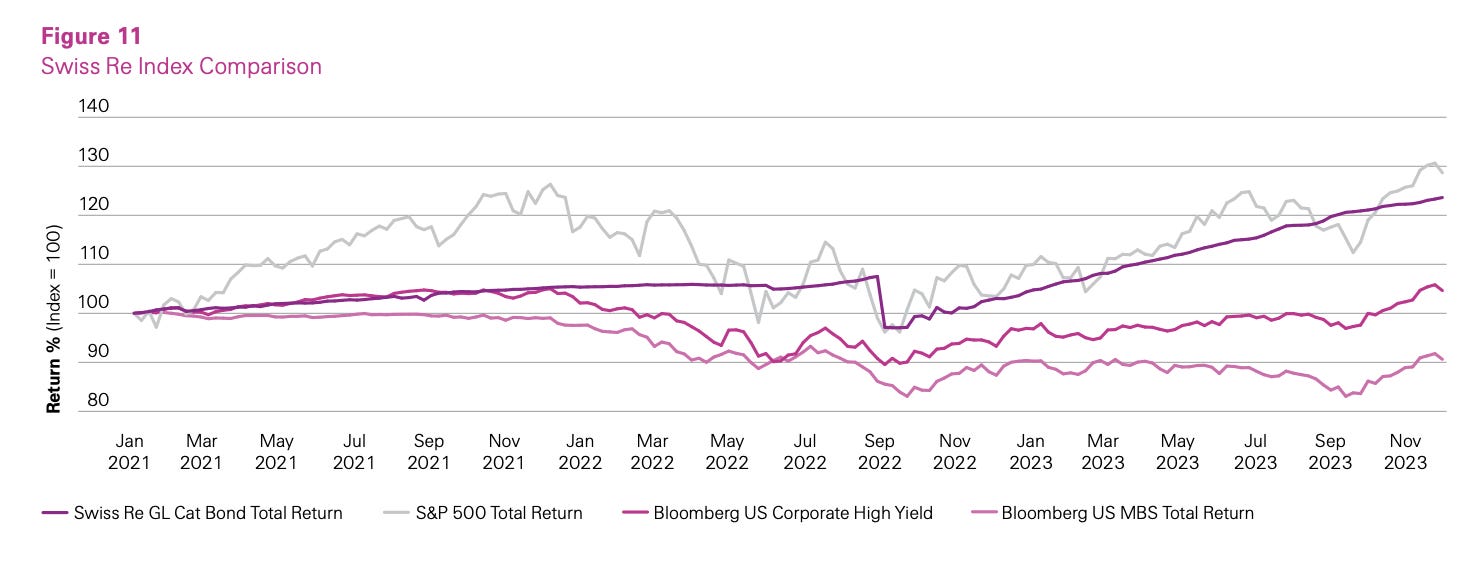

As extreme weather events intensify in volume or severity, the economic impact of natural disasters will grow less isolated. Comparing the gray and purple lines below from the annual report of one of the oldest cat bond sellers, catastrophe returns may imperfectly track the S&P 500 returns, but they’re far from uncorrelated.

While the hedge funds and investment firms buying up cat bonds claim to use advanced modeling to evaluate the true worth of each bond, they primarily rely on only two firms to supply global weather risk data: RMS and AIR. RMS’ parent company Moody’s was one of the most destructive players in the 2008 financial crisis, and the concentrated ownership of risk data makes the possibility of a cat bond bubble all the more alarming.

When news of a disaster circulates, hedge fund managers at Fermat, with stakes in 80% of all cat bond instruments, immediately try to sell off the threatened cat bonds to investors with less information, or a high risk appetite. This passing of the buck gives bondholders one last chance to profit off of their investment, this time betting on the disaster, rather than against it.

Though cat bond strategies posted 20% year-over-year returns last year, the inflows of cash have driven down return rates on this risky asset in the past decade. While some firms are introducing better sensors to solve problems in the field, others rely on remote, 3rd-party data that could lead them astray when things get dicey.

As this new asset class of catastrophe bonds and insurance-linked securities (ILS) grows alongside climate risks, will we leverage finance and technology to protect our communities, or will these bonds perpetrate a catastrophe of their own?

The Closer

The Law of the Sea gives a nation autonomy over marine resources within its exclusive economic zone (EEZ). This coral reef in Kimbe Bay is included in the EEZ of Papua New Guinea. Photograph by David Doubilet, National Geographic