🌐 Could you invest $33B?

(140) dude, chemistry!

Good Morning

What we’re reading this week:

Why recycling alone can’t power climate tech (TR)

HSBC & Google Cloud: Supporting Climate Tech Startups (FT)

Thermal energy storage is poised for a breakout year (HM)

“The Daily” runs greenwashing oil & gas biz ads (H)

The Greendicator

Top Deals of the Week

Koloma, a 10-year-old Denver startup that locates and produces geologic hydrogen, raised a $245 million Series B round led by Khosla Ventures. Axios has more here.

Heura Foods, a seven-year-old Barcelona startup that specializes in creating plant-based meat alternatives inspired by Mediterranean flavors, raised a $43 million Series B round. Investors included Upfield (V)

Indian electric two-wheeler startup River raised a $40M Series B led by Yamaha Motor (TC)

Avnos, a startup developing hybrid direct air capture technology, raised a $36M Series A led by NextEra Energy Resources (BW)

Thea Energy, a startup using software to build reliable and inexpensive fusion power plants, raised a $20M Series A led by Prelude Ventures (TC)

Amperesand, a startup building a silicon-carbide solid-state transformer for a better energy grid, raised a $12.45M seed round led by Xora Innovation and Material Impact (TC)

Volta Insite, an electrical data collection and power quality monitoring startup, raised a $7M seed round (VC)

Green chemistry startup (for applications in pharma) DUDE CHEM raised a $7.1M seed round led by Vorwerk Ventures and b2venture (EU)

EV fleet management startup Guided Energy raised a $5.2M seed round from Sequoia and Dynamo Ventures (TC)

Cosmic Aerospace, a Denver startup that is developing an all-electric passenger aircraft, raised a $4.5 million seed round. Pale Blue Dot was the deal lead (TEU)

Clean chemistry startup AZUL Energy (they make a substitute for rare earth metals used in key clean energy industry technologies) raised a $3.2M Series A led by Spiral Capital (BW)

Green Theory

Could you sustainably invest $33B?

If you had 30 minutes to spend $30, you could probably find an effective allocation for that cash.

What about $33 billion—would you need 33 billion minutes (600 centuries)?

That’s where climate tech investors find themselves: they have so much money (about $33B) that they don’t know what to do with it. With such desperate societal needs for physical and digital green tech deployment, what’s the holdup in investing these sustainable dollars?

Let’s recall the two main ways sustainable investment funds function. The simplest strategies could be summed up as: sell the bad, and buy the good. Barclays (a global British bank) grabbed headlines when they announced plans on both fronts.

The bank outlined enhanced level of divestment from oil and gas projects in early February, including a commitment to “no longer provide project finance, or other direct finance to energy companies, for new upstream oil and gas projects or related infrastructure.” This change represents a huge shift for the fossil funding market, as Barclays has deployed more fossil fuel capital than any other European bank since 2015—a sum totaling nearly $167 billion.

In this new restriction on their investment strategy, a traditional source of reliable returns for the bank will go dry. Where should Barclays invest this freed-up capital? Unlike other banks divesting from fossil fuels, Barclays also released a buy the good plan: rolling out a $1 trillion investment fund for climate solutions and the energy transition over the next 7 years.

The question remains, how should an institution invest any given amount of dollars in climate?

Not enough green opps

While we may desire an acceleration in both types of sustainable investment strategies, there are only so many sustainable investment opportunities available today. As Nat Bullard discusses with Shayle Kann, just because a university endowment or private equity firm decides to divest from fossil fuels today, we can’t expect those freed dollars to chase climate-specific opportunities. Divesting from oil and gas often looks like investing more in healthcare, for instance.

Since building sustainable infrastructure usually requires more capital upfront, in exchange for savings over time (compared to less sustainable alternatives), it’s no wonder that higher economy-wide costs of borrowing are sending a negative ripple effect through climate finance. Buy the good is getting harder in climate.

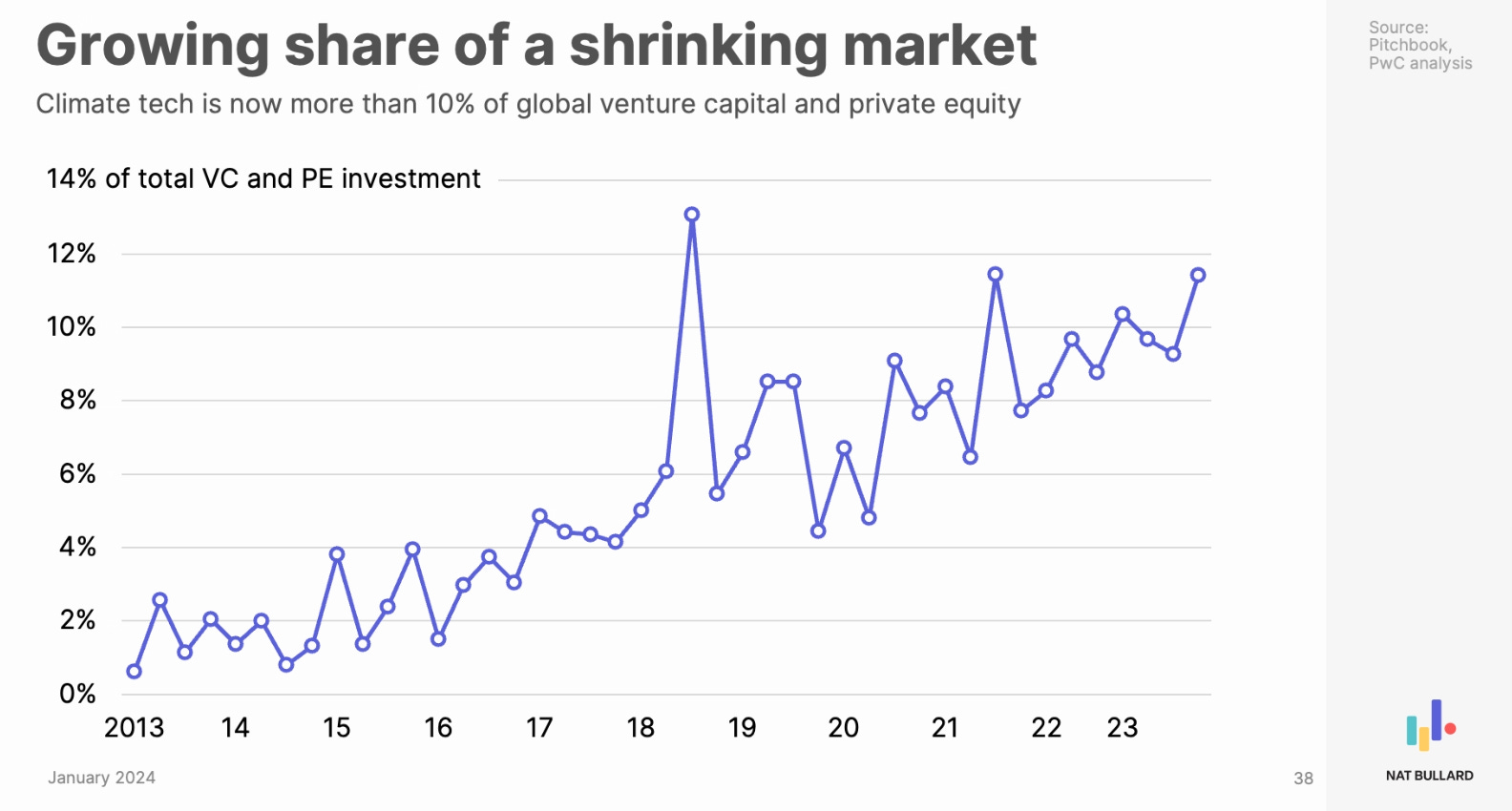

As these two slides in Nat Bullard’s annual report demonstrate (above), the lowest interest rates today hover over 5%, bringing the financing share of new solar and wind to over one third of lifetime costs. This pressure lowers the value of many sustainable investment opportunities, pushing some projects and companies out of profitability. Now, despite the growing number of sustainable dollars, those dollars are chasing fewer viable green investments than 2021 would have forecast.

Hordes of Cash

Just because interest rates dampen some climate solutions, funding of sustainable investment strategies keeps growing. Despite the dramatic shifts in rates over the last 4 years, there’s one climate tech investing trend that keeps innovators’ hopes high, or at least alive: “dry powder.” Reflecting the broader venture capital-wide trend, climate tech venture funds are getting bigger, but also slower.

Dry powder is simply a slang term for readily investable funds. Right when a new venture capital (VC) or private equity (PE) fund is announced, there’s typically some lag between getting the ‘cash’ together and investing it in assets, such as startups. This next step of investing is also called “deploying capital,” and until the capital is deployed, every finance-type seems to need to refer to this money as gunpowder.

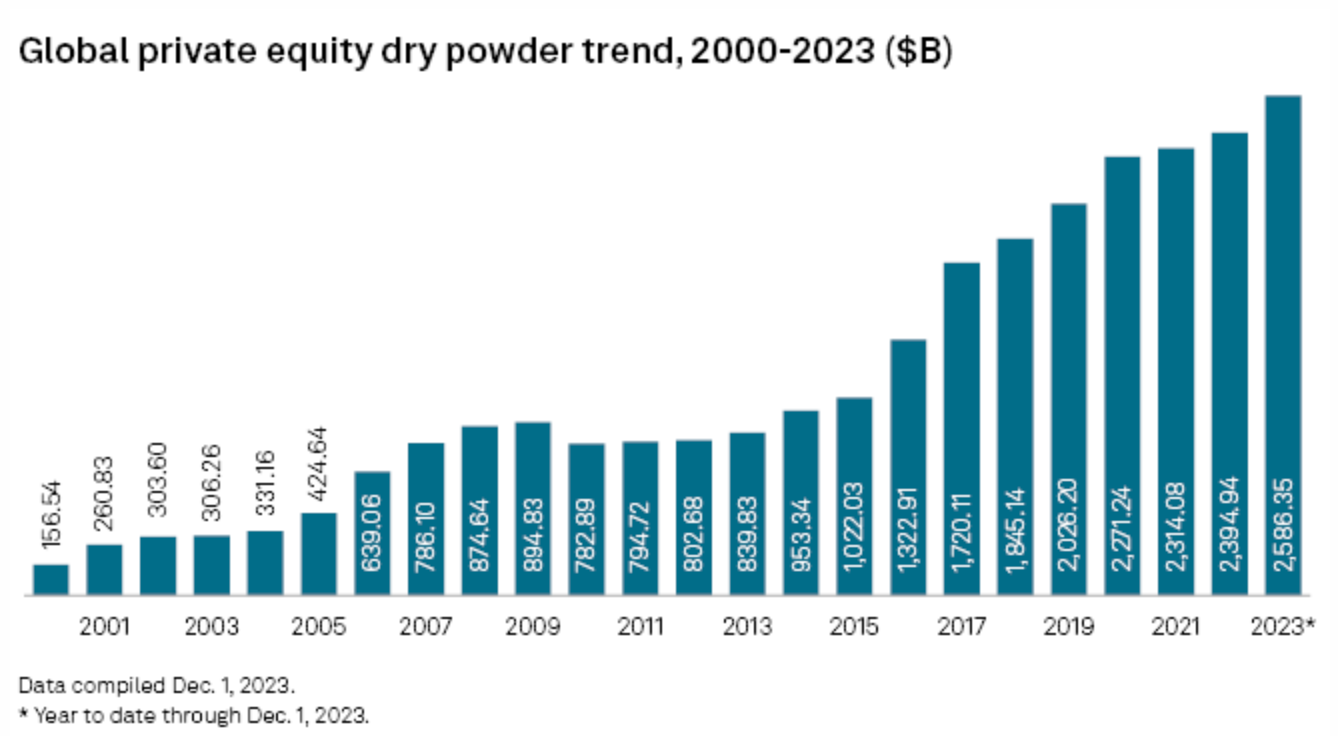

As data from Sightline Climate illustrates, nearly every quarter or half year since we started the Green Bite offered new heights of undeployed cash in climate tech funds. The headline, ‘unprecedented levels of climate tech dry powder,’ showed up again and again in the last 3 years. When we step back to look at the broader economy, such as the global PE undeployed funds (below), or US VC undeployed funds, we also see increasing sums of dollars, slower to get to startups.

The doom loop of undeployed funding

Funds slow down deployment for several reasons. First, these funds are structured to operate over multi-year, even multi-decade time horizons, and if they see brighter general conditions around the corner, firms will be more cautious to invest today. On top of that, sitting on cash can provide emergency funds to prevent a liquidity crisis. In other words, if firms sense a coming recession, keeping a cash cushion creates a hedge. None of this helps today’s startups make payroll.

Still, funds can’t sit on cash forever: their job is to evaluate effective uses of money. This necessity brings up the other reason to slow down deployment, besides macro trends. If the individual investment opportunities (e.g., startups) aren’t appealing, funds must wait on more data from existing startups to validate hypotheses, or for new startups to be founded, before betting (investing).

In some ways, these challenges are inseparable. Tighter macro conditions make more startups look bad to investors, and higher costs of capital make it harder for startups to deliver macro relief to the economy. At the same time, the changing structure of private fund markets is introducing yet another deployment strain, specifically on mid-to-large rounds in tech—and it’s hitting climate tech, too.

Big funds, little returns

Though many systems of markets reward the largest players with the largest rewards, there are limits to scale, and some financial strategies get significantly worse as they grow in dollar size. More money, as it stands here, more problems.

Megafunds are a growing trend in tech investing: with large corporations building out venture wings, and wealthy individuals using their clout to attract new big-ticket investment partnerships.

In climate tech investing, about 70% of the dollars are managed by less than 20% of the investors, each with over $500 million in assets under management. These larger funds necessarily need to find more dollars’ worth of opportunities, and therefore often compromise on the quality of the opportunities they back. Otherwise, they must sit and wait to deploy, and this choosiness deepens the dry powder reserves.

Dealflow on the other, small end of the spectrum supports the theory blaming the backup on megafunds, at least in part. Tons of new, small climate investment funds are popping up. Even though these funds make up a relatively small portion of climate VC dollars, they are deploying capital faster. We see this manifested in seed climate tech investment growing in absolute terms, while most all other tech investing fell year-over-year in 2023.

The macro and the mega: next steps for climate investment

For private capital deployment to speed up in climate tech, do we simply need lower interest rates? If so, lobbying the US Federal Reserve would be among the most essential climate tech needs of 2024.

Luckily, there are other options for innovation besides that one lever. Connecting megafunds with better-diligenced deals, standardizing first-of-a-kind renewable project finance, and founding more relevant climate startups all number among the chances to draw out more of the growing investment reserves, faster.

Innovators need capital, and funds need solutions to invest in. Even with 2024 marking the end-of-runway for many climate tech startups, there is so much money waiting for the right climate opportunities: at least $33 billion, by Sightline’s count.

Will you spend 2024 strengthening a climate company’s value proposition, or refining an actionable sustainable investment thesis? On both sides of the negotiating table, we need climate visionaries and dealmakers to accelerate the energy transition, regardless of what the Fed does.

The Closer

Ah-Shi-Sle-Pah Wilderness Study Area, New Mexico, courtesy of the US Interior